Elderly couple reviewing Medicare and Medicaid cards and medical documents at kitchen table with relieved expressions

Can You Have Both Medicare and Medicaid at the Same Time

Content

Content

Here's something most people don't realize: roughly 12.5 million Americans currently use Medicare and Medicaid together—that's one in five Medicare enrollees. If you're struggling to afford Medicare's premiums and copays while living on a fixed income, you might already qualify for this double coverage without even knowing it.

When you hold both programs (healthcare professionals call this "dual eligible" status), your medical bills essentially disappear. Medicaid picks up what Medicare doesn't pay—those annoying deductibles, the 20% coinsurance, even your monthly premiums. Better yet, you gain access to services Medicare flat-out refuses to cover, including extended nursing home stays and dental work.

This isn't some obscure loophole. It's a legitimate combination designed specifically for low-income seniors and disabled adults who'd otherwise choose between medication and groceries. Let me walk you through exactly how this works, who qualifies, and how to get enrolled.

What It Means to Be Dual Eligible

Think of dual eligibility as layering two different insurance policies that complement each other perfectly.

You've got Medicare—the program most Americans 65+ can access based on their work history or disability status, regardless of how much money they have. Then there's Medicaid, which bases eligibility entirely on your financial situation: low income and minimal assets.

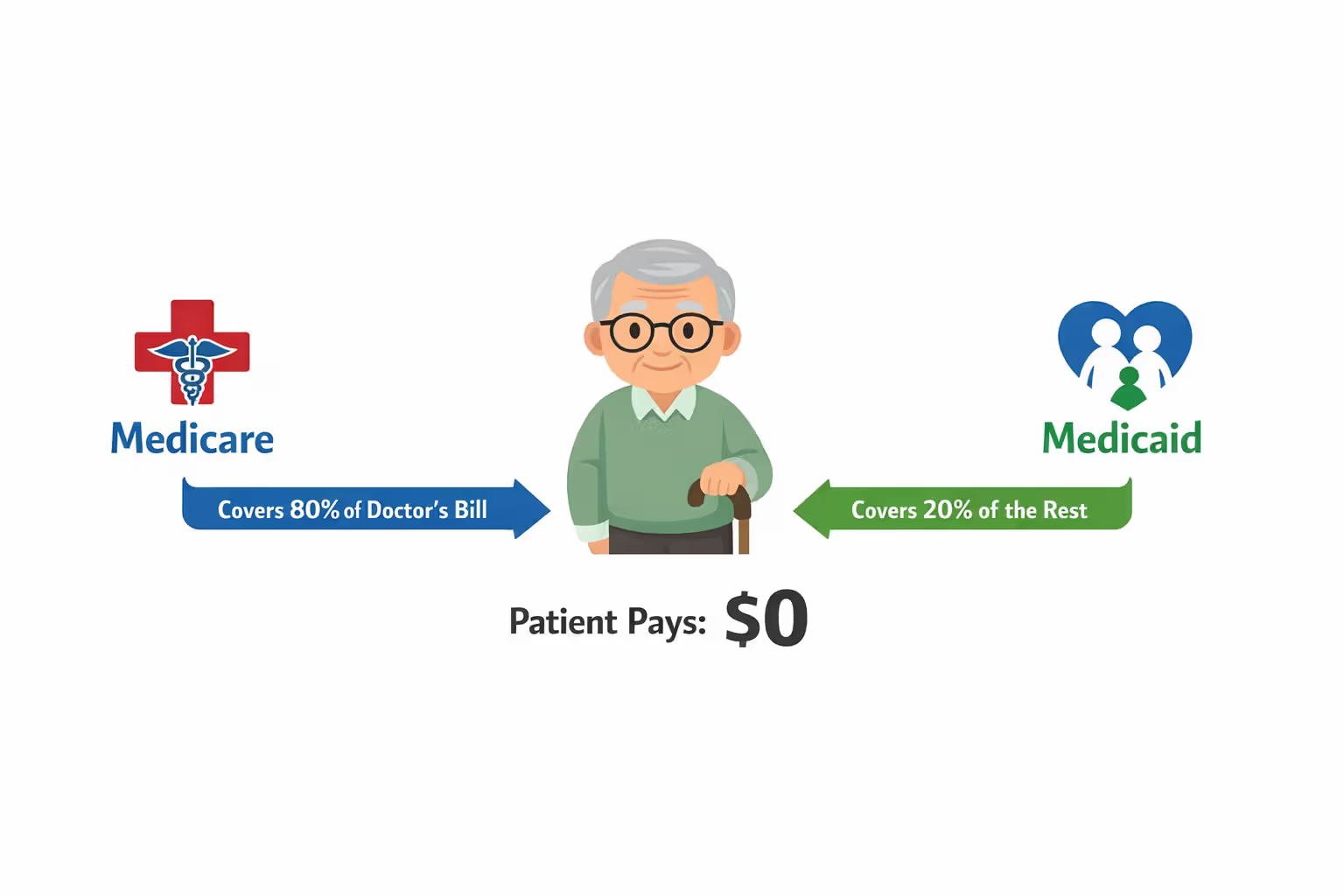

Here's where it gets interesting. When you carry both cards, Medicare always bills first for covered services. A doctor visit? Medicare pays its usual 80%. Then Medicaid automatically covers that remaining 20% you'd normally owe. The same pattern applies to hospital stays, lab work, and prescriptions. You're left paying basically nothing out of pocket.

Author: Ethan Bradford;

Source: proactive-coach.com

Medicaid does something else crucial—it pays your Medicare premiums. Most people see $174.70 deducted from their Social Security check each month for Medicare Part B in 2026. Dual eligibles? That money stays in their account because Medicaid sends the payment to Medicare directly.

The system recognizes three distinct dual-eligible categories. Full dual-eligibles receive comprehensive Medicaid benefits plus Medicare. Partial dual-eligibles qualify for Medicare Savings Programs that handle some (but not all) Medicare costs. Then there's the QMB-only group, who get help exclusively with Medicare's premiums and cost-sharing but don't access broader Medicaid services like dental or nursing home care.

Who Qualifies for Dual Eligibility

Getting dual coverage means clearing two separate hurdles—one federal, one state-based.

Medicare's bar is straightforward: turn 65, or qualify through disability (specifically, collecting Social Security Disability Insurance for two years), or have end-stage kidney disease requiring dialysis. If you've worked at least 10 years paying Medicare taxes, your Part A coverage costs nothing. Worked less? You can still buy in.

Medicaid's requirements get trickier because your state writes its own rulebook within federal boundaries. You'll need limited monthly income and few countable assets—but "limited" means different dollar amounts depending on where you live.

Your house doesn't count toward asset limits. Neither does one car, your furniture, or that modest life insurance policy. States want to know about your bank accounts, investment portfolios, and additional properties. Most cap countable assets at $2,000 for individuals, though some states allow considerably more.

Income and Asset Limits by State

Check out how much qualifying income varies by location for 2026:

| State | Individual Monthly Income Limit | Couple Monthly Income Limit | Asset Limit (Individual) |

| California | $1,732 | $2,338 | $2,000 |

| New York | $1,677 | $2,268 | $31,175 |

| Texas | $1,255 | $1,699 | $2,000 |

| Florida | $1,255 | $1,699 | $2,000 |

| Pennsylvania | $1,732 | $2,338 | $8,000 |

| Illinois | $1,732 | $2,338 | $17,500 |

| Ohio | $1,732 | $2,338 | $2,000 |

| North Carolina | $1,255 | $1,699 | $2,000 |

Notice New York's dramatically higher asset limit? That's why researching your specific state matters. These figures apply to the aged, blind, and disabled Medicaid categories—the pathways most dual-eligibles use. Income thresholds adjust annually tracking federal poverty guidelines.

Special Eligibility Categories

You don't necessarily need full Medicaid to get help with Medicare costs. Several "partial" programs exist with more generous income ceilings.

The QMB program accepts applicants earning up to 100% of the federal poverty level (about $15,060 for individuals in 2026). SLMBs can earn between 100% and 120% of poverty level. The QI category stretches to 135% of poverty level, though Congress funds it year-to-year with limited slots.

Disabled workers face a catch-22: earning too much money disqualifies them from Medicaid, but they need that income to survive. Many states now offer Medicaid Buy-In programs letting disabled individuals maintain coverage despite higher earnings from employment. You essentially pay a premium based on your income, but keep your Medicaid card.

How Medicare and Medicaid Work Together

The payment sequence matters more than you'd think. Medicare must process claims first—always, no exceptions. Then Medicaid reviews what Medicare paid and covers allowable remaining costs.

Let's say you need emergency surgery. Medicare Part A covers your hospital stay minus a $1,676 deductible (that's the 2026 amount). As a dual-eligible, Medicaid pays that deductible. If your stay extends beyond 60 days, Medicare's daily coinsurance kicks in. Again, Medicaid covers it. You sign nothing, write no checks—the programs coordinate automatically behind the scenes.

Doctor visits follow similar logic. Medicare Part B pays 80% after you've met your annual $257 deductible. Medicaid handles the deductible plus that 20% coinsurance. Healthcare providers who accept Medicare must accept Medicaid's payment as full compensation—they're legally prohibited from billing you the difference.

Medicare Savings Programs create a middle tier for people who don't quite qualify for full Medicaid. The QMB level covers every Medicare premium, deductible, and copay. SLMB beneficiaries get only their Part B premium covered—currently $174.70 monthly. The QI program mirrors SLMB but operates on first-come funding that expires each calendar year.

Prescription coverage through Part D becomes ridiculously affordable. Where regular Medicare enrollees might pay $50+ monthly premiums and face that infamous coverage gap, dual-eligibles pay maximum copays of $4.50 for generics and $11.20 for brand names in 2026. Those copays apply all year with no gap period.

Here's a mistake I see constantly: beneficiaries trying to choose which program pays first for different services. You can't. Federal law mandates Medicare primary status for all Medicare-covered services. Providers who bill Medicaid first trigger claim rejections and payment delays lasting weeks.

Author: Ethan Bradford;

Source: proactive-coach.com

Benefits of Having Both Programs

Let's talk actual dollars saved. A Medicare-only beneficiary pays $2,096.40 annually just in Part B premiums. Add a typical $3,000 Part A hospital deductible, various copays for specialists, and a modest $600 Part D premium—you're looking at $6,000+ in annual costs before receiving a single service. Dual-eligibles? Zero. Nothing.

That difference alone keeps countless seniors housed and fed.

But cost elimination barely scratches the surface. The real advantage shows up in coverage breadth.

Medicare covers up to 100 days in skilled nursing facilities—but only when you're recovering from a hospital stay and need daily skilled care. Once those days expire or you no longer need skilled services, Medicare stops paying. Medicaid has no such limits. If you need custodial nursing home care (help with bathing, dressing, eating), Medicaid covers indefinite stays. This single benefit protects families from financial devastation that nursing home bills create.

Most people discover too late that Medicare doesn't cover routine dental work. No cleanings, no fillings, no dentures—unless it's emergency jaw surgery, you're paying out of pocket. Medicaid fills this gap in most states. Exactly what's covered varies (some states offer only emergency dental), but dual-eligibles at minimum get extractions and pain relief. Many states now cover preventive care and dentures.

The same pattern applies to vision care. Medicare covers eye exams only when you've got a specific disease like glaucoma or diabetes affecting your vision. Need reading glasses? Too bad. Medicaid in most states covers one pair of glasses annually plus routine eye exams.

Transportation becomes huge for elderly patients without cars or mobility issues. Miss your dialysis appointment because you can't drive? Medicaid arranges medical transportation in most states—actual vehicles that pick you up, take you to appointments, and bring you home. Medicare doesn't offer this.

Perhaps most valuable for maintaining independence: Medicaid funds home health aides and personal care attendants. These aren't nurses providing wound care (Medicare covers that briefly). These are caregivers who help you bathe, prepare meals, do laundry—the daily living tasks that determine whether you can stay home or must enter a facility. Medicaid waiver programs in every state now prioritize keeping beneficiaries in their homes rather than institutions.

Dual eligible beneficiaries represent some of the most medically complex and economically vulnerable individuals in our healthcare system. The coordination between Medicare and Medicaid isn't just about reducing costs—it's about ensuring that serious illness doesn't force people into impossible choices between medical care and basic necessities like food and housing.

— Dr. Patricia Morrison

How to Apply for Dual Eligibility

You're essentially running two applications on parallel tracks since no unified dual-eligibility application exists.

Author: Ethan Bradford;

Source: proactive-coach.com

The Medicare piece often happens automatically. Already collecting Social Security when you turn 65? Your red, white, and blue Medicare card arrives in your mailbox about three months before your birthday month. You don't request it—Social Security enrolls you automatically in both Part A and Part B.

Not collecting Social Security yet? You've got a seven-month Initial Enrollment Period centered on your birthday month. Miss this window and you'll pay lifetime late penalties on your Part B premium. You can enroll online at ssa.gov, by phone, or at any Social Security office.

Medicaid never enrolls you automatically (with one exception I'll mention). You must contact your state Medicaid agency and submit an application. Every state maintains an online portal—search "

Medicaid application." You can also apply by phone, mail, or in person at local Medicaid offices (often called Department of Social Services or Department of Health and Human Services).Gather these documents before starting: government-issued ID, Social Security card, proof you live in the state (utility bill, lease, mortgage statement), three months of bank statements for all accounts, documentation of all income sources (Social Security award letter, pension statements, pay stubs if working), and your Medicare card if already enrolled.

Applications typically take 45 to 90 days for processing, though I've seen variations from 30 days to four months depending on state workload and how complete your application was. You'll receive a written determination explaining your approval or denial. Approved? Your Medicaid card arrives separately, and you can start using both programs immediately.

Denials don't mean game over. Request an appeal within the timeframe specified in your denial letter (usually 30 to 90 days). Many initial denials stem from missing paperwork rather than actual ineligibility. A benefits counselor can review your denial and help gather necessary documentation.

One automatic enrollment exception exists: SSI recipients. If you collect Supplemental Security Income, most states automatically enroll you in Medicaid without requiring an application. You'll still need to enroll in Medicare separately, but the Medicaid piece happens automatically.

Moving states creates a trap. Your Medicaid coverage doesn't transfer. You must apply fresh in your new state, which might use completely different eligibility rules. I've seen people move from generous states like New York to restrictive states like Texas and lose eligibility entirely. Notify both states immediately when relocating to minimize coverage gaps.

Maintaining Your Dual Eligibility Status

Getting approved is step one. Staying enrolled requires ongoing attention.

Medicare continues indefinitely once you're enrolled—no annual renewal needed. Medicaid operates differently. Most states require annual recertification, sending you a renewal packet two to three months before your coverage expires. This packet asks essentially the same questions as your initial application: current income, assets, household composition, living situation.

Return this packet promptly with updated documentation. Even if nothing changed, states need current bank statements and income verification. Many states now use "ex parte" reviews, checking databases electronically before requesting documentation from you. If their systems verify continued eligibility, you might complete renewal without submitting anything.

Author: Ethan Bradford;

Source: proactive-coach.com

Missing your renewal deadline terminates coverage. You'll need to reapply from scratch, facing that 45-to-90-day processing window again. During this gap, you're stuck paying Medicare's full cost-sharing.

Income changes require immediate reporting in most states—usually within 10 days. "Changes" means starting or stopping work, getting a raise, changes in Social Security payments, receiving an inheritance, or winning significant gambling proceeds. Don't panic over tiny fluctuations. Your annual Social Security cost-of-living adjustment won't disqualify you because Medicaid's income limits adjust proportionally.

Asset changes matter too. Inherited $50,000? Report it. Sold your second property? Report it. But spending assets strategically can maintain eligibility: paying off your mortgage, making necessary home repairs, buying a burial plot, or purchasing a Medicaid-compliant annuity. A benefits attorney can explain spend-down strategies.

Losing Medicaid doesn't terminate Medicare. They're separate programs with independent eligibility rules. But losing Medicaid means those premiums, deductibles, and copays suddenly become your responsibility. You might still qualify for a Medicare Savings Program even without full Medicaid—worth exploring before accepting full cost-sharing burden.

Regaining eligibility after loss requires submitting a completely new application. No expedited process exists. You're looking at normal processing times, potentially creating a coverage gap lasting months.

Common Questions About Dual Eligibility

Conclusion

Carrying Medicare and Medicaid simultaneously transforms healthcare from a financial stress into a manageable reality. You eliminate thousands in annual premiums, deductibles, and copayments while gaining coverage for services Medicare completely ignores—particularly extended nursing home stays, dental work, and vision care that matter enormously for quality of life.

Qualification hinges on meeting Medicare's age or disability standard while your income and assets fall within your state's Medicaid thresholds. You'll navigate two separate application processes since no unified enrollment exists. Maintaining coverage demands annual Medicaid renewals and promptly reporting financial changes.

This combination creates a comprehensive safety net allowing millions of low-income seniors and disabled adults to access necessary medical care without choosing between treatment and groceries. If your income and assets fall near qualifying levels, the application effort pays off dramatically in reduced costs and expanded coverage.

Start by calling your state Medicaid office (find the number by searching "Medicaid contact"). Ask specifically about aged and disabled Medicaid programs and Medicare Savings Programs. If you're slightly above income limits, discuss spend-down provisions or special eligibility pathways that might apply to your circumstances. Free counseling through State Health Insurance Assistance Programs (SHIP) can help you understand options and complete applications. The financial relief and coverage expansion make pursuing dual eligibility worth every minute spent on paperwork.

Related Stories

Read more

Read more

The content on this website is provided for general informational and educational purposes only. It is intended to offer guidance on pet insurance topics, including coverage options, deductibles, premiums, claims processes, reimbursement models, waiting periods, and related insurance matters. The information presented should not be considered legal, financial, veterinary, or professional insurance advice.

All information, articles, explanations, and policy discussions published on this website are provided for general informational purposes. Pet insurance policies vary widely between providers, and details such as coverage limits, exclusions, reimbursement rates, waiting periods, pre-existing condition policies, pricing, and eligibility requirements may differ depending on the insurer, pet breed, age, location, and the specific terms of an individual policy. Claim outcomes and reimbursement decisions depend on the exact policy language and the circumstances of each case.

While we strive to keep the information accurate and up to date, this website makes no guarantees regarding the completeness, reliability, or accuracy of the content. The website and its authors are not responsible for any errors, omissions, or actions taken based on the information provided here.

Use of this website does not create a professional-client relationship. Pet owners are encouraged to review the official policy documents provided by insurance companies and consult with a licensed insurance professional or qualified veterinarian when making decisions about pet insurance coverage and care for their pets.