Happy diverse family with two children visiting pediatrician in modern medical office, doctor in white coat talking to child, health insurance card on desk

CHIP Health Insurance Guide for Families

Content

Content

When your household brings in too much for Medicaid but not enough to comfortably pay $800 monthly premiums for family coverage, where do you turn? The Children's Health Insurance Program fills exactly this gap—giving working families access to quality pediatric care without choosing between medical bills and groceries.

What Is CHIP Health Insurance?

Think of CHIP as the middle ground between Medicaid and private insurance. Created by Congress in 1997, this program targets a specific group: families whose paychecks disqualify them from traditional Medicaid yet can't realistically afford employer plans or marketplace policies.

Here's how it works structurally. Washington provides the framework and funding—covering 65% to 88% of costs depending on each state's wealth—while individual states design and run their own versions. That's why you'll see different names across the country. Georgia calls theirs PeachCare. Indiana uses Hoosier Healthwise. New York went with Child Health Plus. Same federal program, fifty different implementations.

The Medicaid comparison trips people up constantly. Yes, both serve lower-income families. But Medicaid operates as an entitlement—if you qualify, you're in, period. CHIP runs on allocated budgets that theoretically could run dry, though Congress keeps renewing funding. More importantly, CHIP accepts families earning 200% to 400% of poverty level income, while Medicaid typically cuts off around 138% to 200% depending where you live.

Who gets covered? Almost exclusively kids under 19. A handful of states extend limited benefits to pregnant women, but this remains primarily a children's program. As of early 2026, roughly 7.2 million kids nationwide carried CHIP cards—that's more than the entire population of Massachusetts.

The program exists because employer insurance became unaffordable for many working families. Adding two kids to a workplace plan might cost $600 monthly after employer contributions. For households earning $45,000 yearly, that's nearly 20% of gross income before a single doctor visit happens.

Who Qualifies for CHIP Coverage?

Four factors determine whether your kids can enroll: how old they are, where you live, what you earn, and their citizenship status. Kids must be under 19, reside in the state where you're applying, and be either U.S. citizens or legally present immigrants. Income creates the complicated part.

Your state sets its own earnings threshold within federal boundaries. Most choose somewhere between 200% and 300% of the Federal Poverty Level—though some go as high as 400%. Translation? A four-person household pulling in $72,000 to $108,000 might still qualify in certain states. That's not poverty by any definition, but it's also not enough to easily absorb $1,200 monthly for family health coverage.

Author: Melissa Grant;

Source: proactive-coach.com

Income Limits by State

Geography matters enormously with CHIP. Check how eligibility shifts across these five states for 2026:

| Family Size | 2026 Federal Poverty Level | California (317% FPL) | Texas (215% FPL) | Florida (211% FPL) | New York (405% FPL) |

| 2 people | $20,440 | $64,795 | $43,946 | $43,128 | $82,782 |

| 3 people | $25,820 | $81,850 | $55,513 | $54,480 | $104,571 |

| 4 people | $31,200 | $98,904 | $67,080 | $65,832 | $126,360 |

| 5 people | $36,580 | $115,959 | $78,647 | $77,184 | $148,149 |

These numbers reflect gross income—what you earn before Uncle Sam takes his cut. States count wages, self-employment profits, Social Security checks, unemployment benefits, and virtually every other income source. A few allow deductions for childcare expenses or disability-related costs, but don't count on it.

Special Eligibility Cases

Several situations bend the standard rules. Kids aging out of foster care can qualify regardless of family income until they hit 26 in states that adopted this option. Lawfully present immigrant children face a five-year waiting period in 15 states, though 35 states plus D.C. eliminated this barrier using their own money.

Children with disabilities sometimes qualify even when family earnings far exceed normal cutoffs, particularly if the child needs institutional-level care. Several states run "buy-in" programs letting higher-income families purchase CHIP coverage at elevated premiums—think $150 monthly instead of $30.

Here's a mistake I see repeatedly: parents assume if their oldest qualifies for Medicaid, the younger kids automatically do too. Wrong. Income brackets sometimes split siblings between programs. A seven-year-old lands in Medicaid while her ten-year-old brother gets CHIP. Apply for both programs at once and let the state sort out who goes where.

How to Apply for CHIP Health Insurance

Most states merged their CHIP and Medicaid applications into one form, so you'll apply through the same channels. Three options exist: online through your state's marketplace or CHIP portal, by phone via your state's enrollment hotline, or old-school paper application dropped in the mail or handed over in person.

Start at HealthCare.gov, punch in your state, and it'll bounce you to the right application portal. Or skip the middleman and Google "

CHIP application" for the direct link. States must process applications within 45 days by federal law, though most finish reviews in two to three weeks.

Author: Melissa Grant;

Source: proactive-coach.com

Round up these documents before starting:

- Recent income proof for everyone in the household (last month's pay stubs, previous year's tax return, self-employment ledgers, unemployment statements)

- Social Security numbers for each person applying

- Immigration paperwork if applicable (green cards, visa documents, naturalization certificates)

- Something proving you live in the state (utility bill, lease, driver's license)

Don't wait for every single paper before hitting submit. Send what you have, then supply the rest when requested. Waiting means delayed coverage—some states even provide temporary enrollment while verifying your information.

How long until you hear back? Depends on state workload and whether your application arrived complete. Incomplete submissions get bounced or stuck in pending status, stretching timelines by weeks. Approval typically means coverage starting the first day of the following month, though some states backdate coverage up to three months if your child qualified during that window.

One timing trick: apply in the last week of any month. Quick processing might start coverage the next month instead of getting pushed to the month after. Got urgent medical needs? Mention it—some states fast-track applications for kids requiring immediate care.

What CHIP Health Insurance Covers

Federal standards mandate certain benefits while letting states pile on extras. Every CHIP plan includes routine checkups, shots, sick visits, prescriptions, dental and vision care, hospital stays (both inpatient and outpatient), lab work, X-rays, and emergency treatment.

Preventive services get special attention. Well-child visits, developmental screenings, hearing tests, age-appropriate vaccines—all typically come with zero copay. The strategy here is catching problems early when they're cheaper and easier to fix.

Dental coverage often beats what private insurance offers. Kids get cleanings, fluoride treatments, sealants, fillings, extractions, and even braces when medically necessary. Vision coverage includes yearly eye exams, glasses, and treatment for eye diseases.

Mental health services fall under the umbrella too—counseling, therapy sessions, psychiatric medications all get covered. Adolescent substance abuse treatment is included, addressing something many private plans either exclude or severely limit.

Prescription medications come from approved lists called formularies. Most common pediatric drugs appear on these lists, though some states want prior authorization for certain medications or push generic versions when available. Copays run $0 to $5 per prescription in most places.

What you won't find covered: cosmetic procedures, experimental treatments lacking pediatric approval, and services deemed medically unnecessary. Some states exclude particular therapies or cap visits for specific services. Adult dental care—even for pregnant women in states covering expectant mothers—receives limited or zero coverage.

Cost-sharing varies by state and earnings. Families above 150% FPL usually pay small monthly premiums—figure $10 to $60 per family total. Copays stay modest: $0 to $5 for doctor visits, $0 to $3 for prescriptions, $15 to $75 for emergency room trips. Annual out-of-pocket limits protect families from catastrophic costs, typically capping expenses at 5% of household income.

We've watched CHIP transform pediatric healthcare for working-class families over the past two decades. Kids now get preventive checkups instead of waiting until they're desperately sick. Asthma gets managed properly rather than sending kids to the ER monthly. Parents stop choosing between their child's strep throat treatment and the electric bill. The health improvements are measurable, but the psychological relief for parents might matter even more.

— Dr. Sarah Martinez

CHIP Renewal Requirements and Deadlines

Your CHIP coverage doesn't last forever—most states require renewal every 12 months, though some check in every six months. Expect a renewal notice in your mailbox 60 to 90 days before your coverage expires, giving you plenty of runway to complete the paperwork and avoid gaps.

The renewal packet shows up with a pre-filled form containing your current information. Double-check every line. Addresses change. Income fluctuates. Household composition shifts. Update anything that's wrong, sign the form, and send it back by the printed deadline. Many states now let you renew online through the same portal you used originally.

Updated income documentation is mandatory at renewal time. Gather recent pay stubs, tax information, or other proof of current earnings. Income went up but stayed within CHIP limits? You're fine. Income dropped? Your kids might shift to Medicaid instead. Income jumped above CHIP thresholds? You'll get notice to find marketplace coverage, usually with a special enrollment period.

Missing the deadline doesn't instantly kill your coverage. Most states grant a grace period—30 to 90 days—where coverage continues while they try reaching you. After that grace period expires, though, coverage stops and you're starting from scratch with a new application instead of simple renewal.

Set phone or calendar reminders for renewal deadlines. Mark the actual deadline, then add alerts 30 and 60 days out. This simple habit prevents the most common CHIP loss reason: forgetting the paperwork deadline rather than actual ineligibility.

Between renewal periods, life changes sometimes require updating your application. Lost your job? Income changed significantly? Moved? Added a new baby? Immigration status shifted? Report these changes within 10 days in most states. They might affect eligibility or benefits, and timely reporting prevents overpayment headaches or sudden coverage drops.

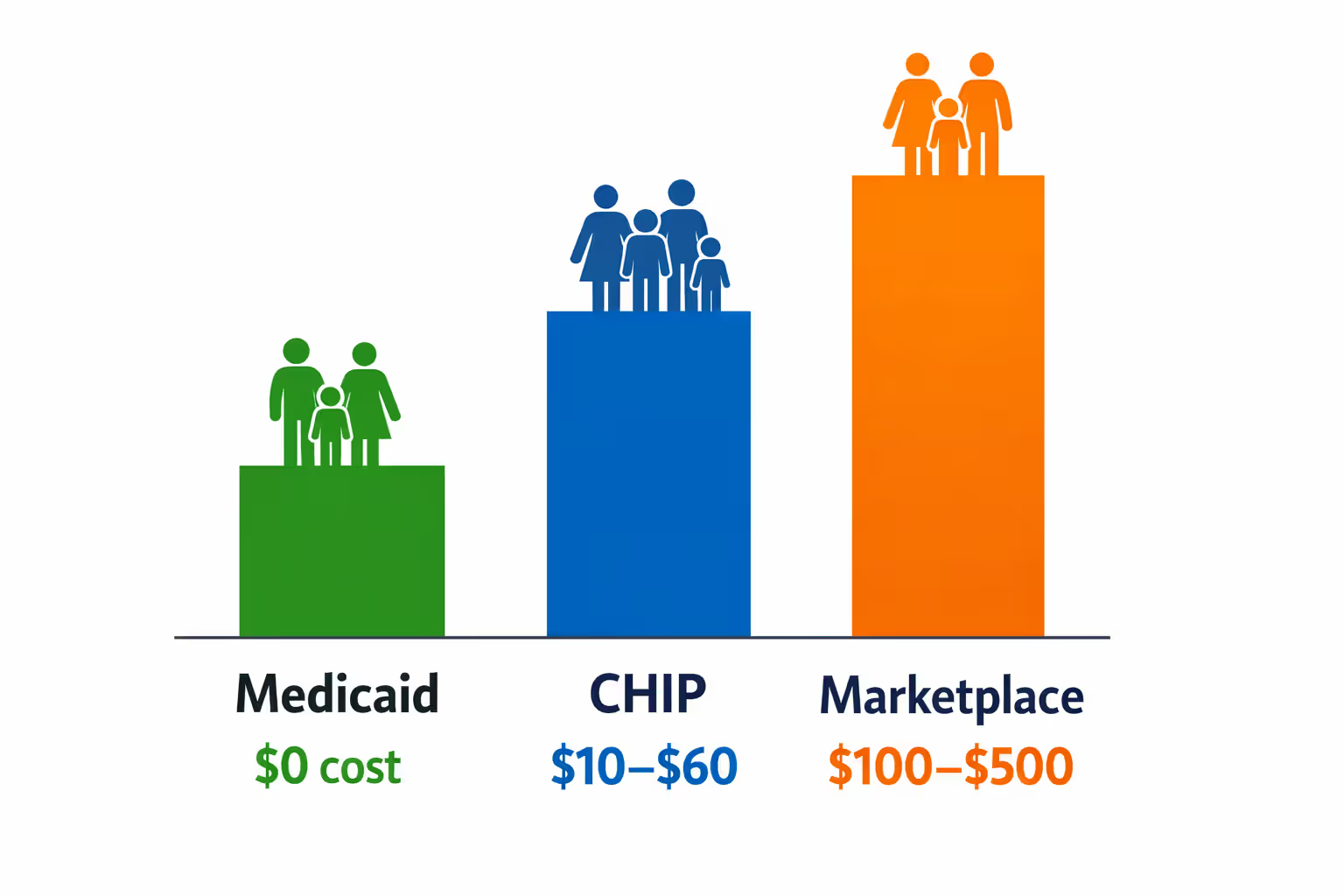

CHIP vs. Medicaid vs. Marketplace Insurance

Income, family makeup, and state-specific rules determine which program fits your situation. Understanding the distinctions helps you pick the right option and avoid falling through coverage cracks.

Medicaid serves children in lower-income families—typically up to 138% to 200% of FPL depending on your state. CHIP catches the next income tier, covering kids in families earning roughly 200% to 400% FPL. Marketplace insurance handles families above CHIP limits, offering subsidized private plans through Affordable Care Act exchanges.

Cost differences are stark. Medicaid charges no premiums and little or no copays. CHIP asks for modest premiums (often $10-$60 monthly) and small copays. Marketplace plans, even subsidized ones, typically run $100 to $500 monthly with deductibles hitting $1,000 to $5,000 before full coverage kicks in.

Medicaid and CHIP benefits are comprehensive and kid-focused. Marketplace plans vary wildly—some offer robust coverage, others feature narrow networks and steep cost-sharing. CHIP and Medicaid guarantee dental and vision coverage; marketplace plans often charge extra for pediatric dental.

Author: Melissa Grant;

Source: proactive-coach.com

Can family members carry different coverage? Absolutely. Parents might buy marketplace insurance while kids get CHIP or Medicaid. This split-family setup is common and perfectly legal. Some families even have one child on Medicaid and another on CHIP based on age or disability factors.

When income hovers near program boundaries, small fluctuations trigger coverage switches. A raise pushing you from CHIP to marketplace insurance might actually cost more in premiums and deductibles than the raise provides in extra income. Some families strategically manage income timing—deferring bonuses or scheduling self-employment income—to maintain CHIP eligibility, though this requires careful planning and honest reporting.

States must provide seamless program transitions. Lose CHIP eligibility due to rising income? You get information about marketplace special enrollment periods. Income drops? The state should automatically move your child to Medicaid without requiring a fresh application.

Frequently Asked Questions About CHIP

Taking the Next Step

CHIP bridges a critical coverage gap for working families—those earning too much for Medicaid yet struggling to afford private insurance. The program delivers comprehensive health, dental, and vision benefits at minimal cost, ensuring millions of children get preventive care, manage chronic conditions, and access treatment when sick or injured.

Eligibility hinges on your state's income limits, your child's age and citizenship status, and family size. Most families earning between 200% and 300% of poverty qualify, with some states extending coverage to 400% FPL. Applications are straightforward, typically taking two to three weeks, and require basic income and residency documentation.

Understanding renewal requirements prevents coverage interruptions—calendar the renewal deadline and update information promptly when circumstances change. Compare CHIP against Medicaid and marketplace options to ensure your family secures the most appropriate and affordable coverage.

Unsure whether your children qualify? Apply anyway. States evaluate eligibility and place children in the appropriate program—Medicaid, CHIP, or marketplace with subsidies. The application is free and takes maybe an hour gathering documents and completing forms. Worst case? You discover your children qualify for affordable coverage you didn't know existed. Best case? Your kids get consistent healthcare without financial stress.

Related Stories

Read more

Read more

The content on this website is provided for general informational and educational purposes only. It is intended to offer guidance on pet insurance topics, including coverage options, deductibles, premiums, claims processes, reimbursement models, waiting periods, and related insurance matters. The information presented should not be considered legal, financial, veterinary, or professional insurance advice.

All information, articles, explanations, and policy discussions published on this website are provided for general informational purposes. Pet insurance policies vary widely between providers, and details such as coverage limits, exclusions, reimbursement rates, waiting periods, pre-existing condition policies, pricing, and eligibility requirements may differ depending on the insurer, pet breed, age, location, and the specific terms of an individual policy. Claim outcomes and reimbursement decisions depend on the exact policy language and the circumstances of each case.

While we strive to keep the information accurate and up to date, this website makes no guarantees regarding the completeness, reliability, or accuracy of the content. The website and its authors are not responsible for any errors, omissions, or actions taken based on the information provided here.

Use of this website does not create a professional-client relationship. Pet owners are encouraged to review the official policy documents provided by insurance companies and consult with a licensed insurance professional or qualified veterinarian when making decisions about pet insurance coverage and care for their pets.