Worried young woman reviewing medical bills and using calculator at kitchen table with laptop and insurance documents

What to Do If You Can't Afford Health Insurance and Don't Qualify for Medicaid

Here's where thousands of Americans find themselves stuck: you earn just enough to disqualify you from Medicaid, yet insurance premiums gobble up such a massive chunk of your paycheck that buying coverage feels impossible. About 2.2 million people wrestle with this exact predicament right now—especially if you live somewhere that rejected Medicaid expansion.

The worst part? People in this situation typically avoid doctors until something breaks. They skip blood pressure checks, ignore that weird lump, stretch insulin doses dangerously thin. Then a medical crisis hits and suddenly they're drowning in five-figure bills. But you've got more options than you probably realize, even when standard insurance channels appear completely blocked off.

Why You Might Not Qualify for Medicaid

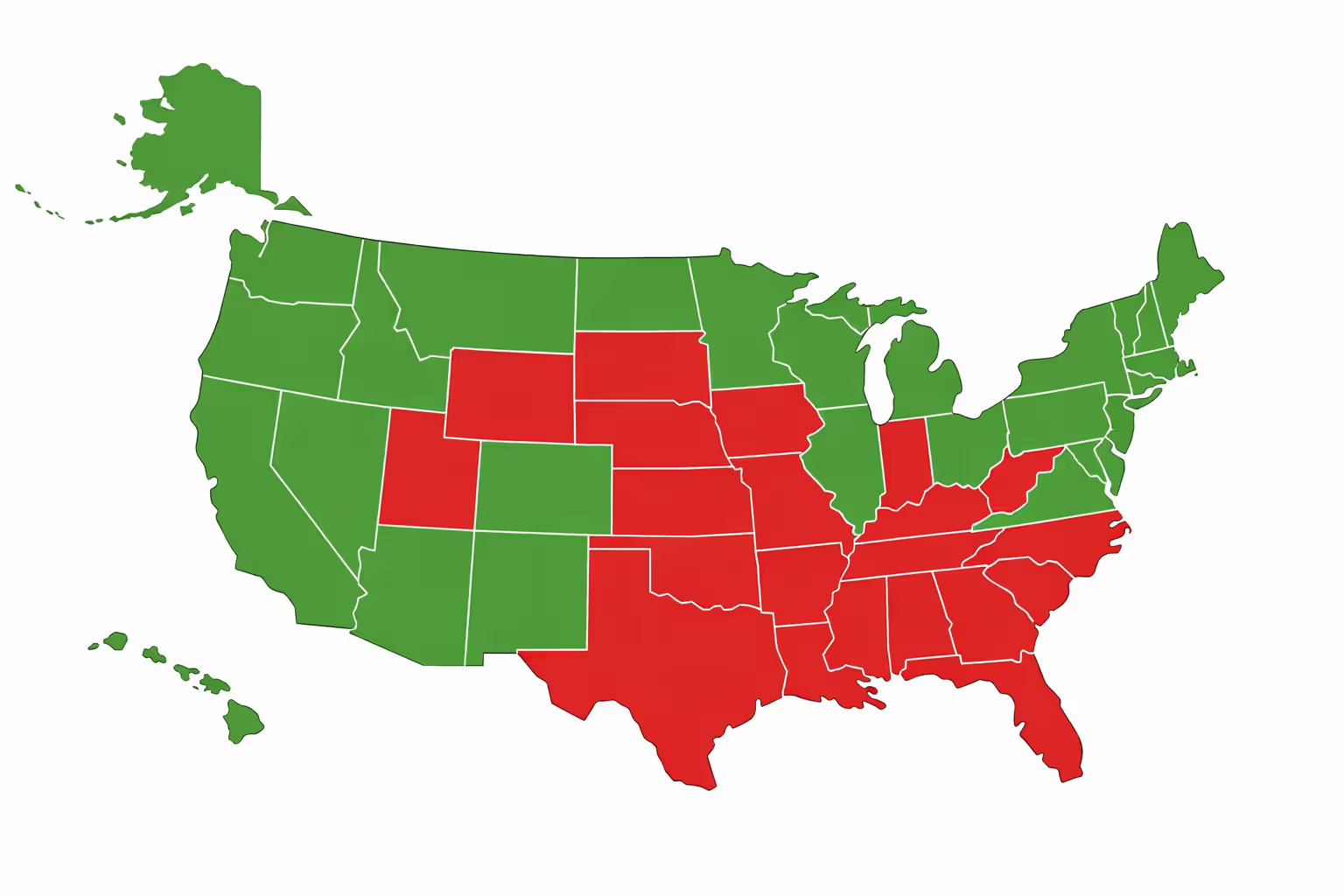

Income caps determine who gets Medicaid, and these thresholds shift wildly depending on which state you call home. The federal government set up baseline rules, then basically told states "do whatever you want" with the details.

States that took the Medicaid expansion deal let adults qualify when they earn up to 138% of federal poverty guidelines. States that refused? They often restrict Medicaid to parents earning poverty-level wages—we're talking 18% FPL in some places—while shutting out childless adults completely, even those living on $10,000 yearly.

Your income isn't the only hurdle either. You'll need citizenship documentation or qualifying immigration papers, proof you actually live in that state, and sometimes you'll face asset limits depending on which coverage category you're applying for. A handful of states have tried enforcing work mandates for adults without disabilities, though courts keep striking these down and policy shifts happen constantly.

Understanding Medicaid Income Limits by State

Where you live determines whether you're covered or completely on your own. Take someone making $20,783 annually. In California or New York? They're getting Medicaid. In Texas or Florida? They're getting nothing—zero coverage—unless they happen to be pregnant, disabled, or raising kids.

Families see even bigger differences. Four people living in an expansion state can access Medicaid with household income reaching $42,275. That same family in a non-expansion state? Parents might need to survive on under $7,600 yearly to qualify. That's below what you'd earn working minimum wage full-time.

Income thresholds get adjusted each year when federal poverty calculations change, but the chasm between expansion and non-expansion states stays fixed. Twelve states continue rejecting expansion, leaving millions of working adults stranded without realistic paths to affordable coverage.

Author: Derek Whitmore;

Source: proactive-coach.com

The Medicaid Coverage Gap Explained

Picture this: you're living in a non-expansion state earning $14,000 yearly. You make too much for Medicaid (which cuts off far below your income), yet you make too little for marketplace subsidies (which don't kick in until you hit 100% FPL). You're literally trapped in a coverage dead zone.

Congress never intended this disaster. When they wrote the Affordable Care Act, lawmakers assumed every state would obviously expand Medicaid. That's why marketplace subsidies start at 100% poverty level—there was supposed to be no gap. Then the Supreme Court ruled in 2012 that states could opt out, accidentally creating this nightmare scenario for low-wage workers.

People caught here face absurd choices: take a slightly better-paying job to reach subsidy territory, deliberately stay underemployed to keep Medicaid, or just roll the dice uninsured. Small business owners and freelancers have it especially rough because fluctuating income constantly bounces them between eligibility categories.

Affordable Health Coverage Options Outside Medicaid

Just because Medicaid rejected you doesn't mean you're paying full freight for marketplace insurance. Subsidies drop costs dramatically once you understand how they actually work.

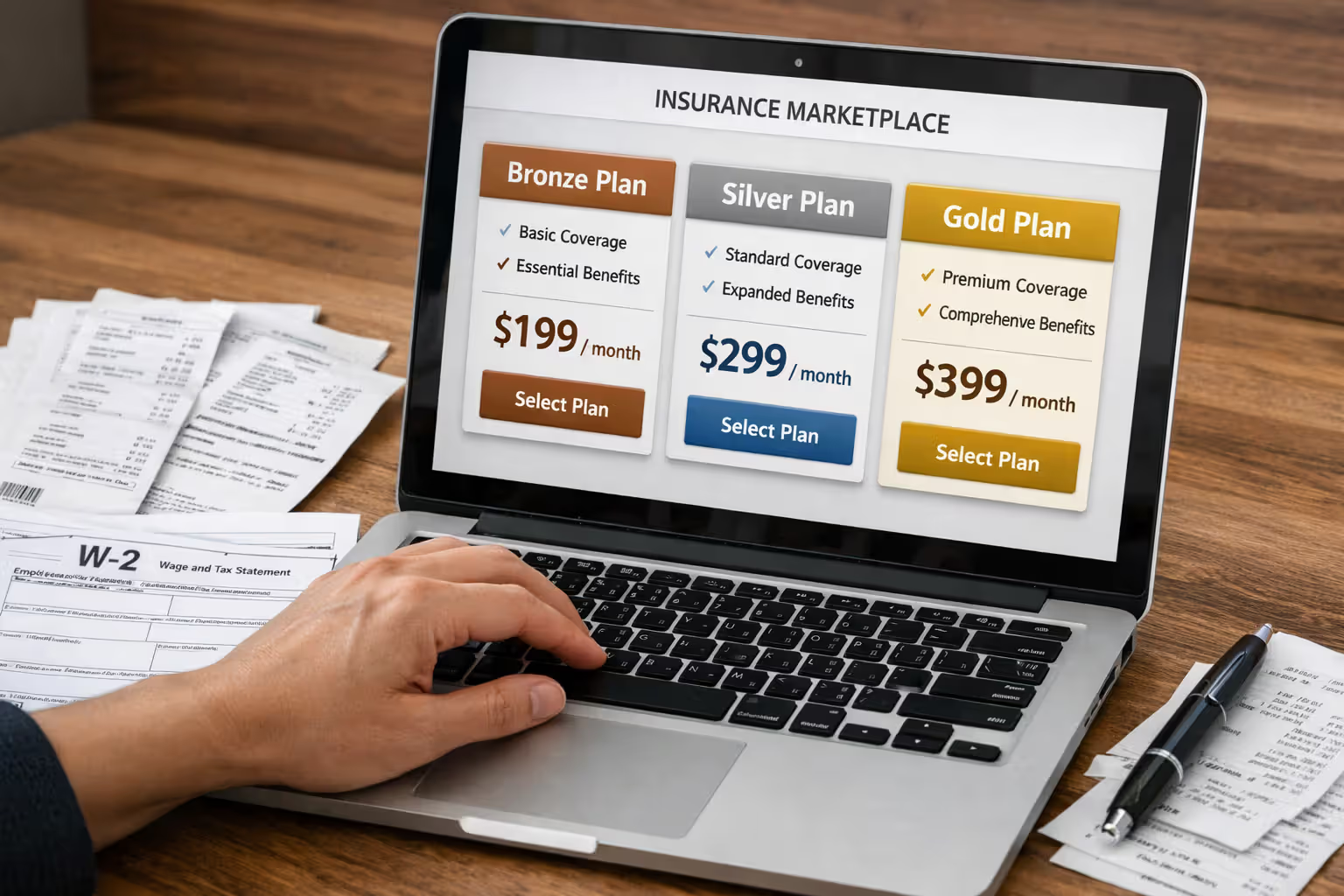

Premium tax credits apply when household income lands between 100% and 400% FPL. Thanks to enhanced subsidies running through 2026, your premium costs max out at 8.5% of what you earn, even if you're above that 400% threshold. Someone pulling in $30,000 yearly might pay $210 monthly for Silver-tier coverage instead of the $450 sticker price.

Cost-sharing reductions sweeten the deal further for anyone under 250% FPL who picks Silver plans. These subsidies slash your deductibles, copays, and out-of-pocket maximums. Instead of facing a $3,500 deductible, someone earning $25,000 might only deal with $500 before insurance starts covering costs. That transforms insurance from theoretical protection into something you'll actually use.

Catastrophic plans work for people under 30 or those qualifying for hardship exemptions. Monthly premiums run cheap—often under $200—but deductibles hover around $9,200. Think of these as financial protection against worst-case disasters. You'll still get three primary care checkups and preventive services covered before hitting that deductible.

Bronze plans split the difference: manageable premiums paired with substantial deductibles. If you're generally healthy and mainly need coverage in case disaster strikes, a subsidized Bronze plan might only cost $50-150 monthly depending on your income and zip code.

Don't guess what you'd pay. Actually plug your numbers into your state's marketplace website. Tons of people assume coverage is unaffordable without checking their real subsidy amounts. Income changes, household size shifts, or even moving across town can completely transform your costs.

Author: Derek Whitmore;

Source: proactive-coach.com

Low-Cost Healthcare Alternatives When Insurance Isn't an Option

When even subsidized premiums stretch beyond your budget, you can still access medical care through alternative channels that won't bankrupt you.

Federally Qualified Health Centers blanket underserved communities nationwide, delivering primary care, dental work, mental health services, and prescription help. They calculate fees based on what you actually earn—some patients pay $20 per visit, others pay nothing. The explicit policy: providers serve everyone regardless of payment ability. More than 1,400 centers currently treat 30 million patients yearly, insured or not.

Free clinics and charitable medical centers fill additional gaps in most cities. Volunteers or nonprofit groups run these operations, handling basic care, chronic disease checkups, and specialist referrals. Quality and hours vary considerably, but they provide crucial access points for adults without coverage.

Direct primary care flips the traditional model. Instead of insurance, you pay your doctor $50-150 monthly for unlimited office visits, extended appointment times, and direct text or email access to your physician. DPC won't cover hospitalizations or specialists, but it handles routine healthcare affordably. Some people pair DPC memberships with catastrophic insurance for comprehensive protection at reasonable total cost.

Prescription assistance programs tackle medication expenses that often devastate uninsured budgets. Drug manufacturers run patient assistance programs offering free or steeply discounted medications based on earnings. Discount programs like GoodRx negotiate pharmacy prices that sometimes run 80% below retail. Health centers frequently operate pharmacies with deeply reduced medication costs.

Nonprofit hospitals must offer charity care programs by law, providing free or discounted treatment for patients below specific income cutoffs—usually 200-300% FPL. Applications typically happen after you receive treatment, though some hospitals accept them beforehand for scheduled procedures. Qualifying patients sometimes see entire bills eliminated.

Urgent care centers increasingly roll out membership programs or transparent pricing for uninsured patients. They cost more than health centers, sure, but they're convenient when you need immediate care for acute illness or minor injuries.

How to Apply for Marketplace Subsidies and Tax Credits

Getting marketplace subsidies means navigating HealthCare.gov or your state exchange during open enrollment periods, unless you qualify for special enrollment. The application determines whether you're eligible and calculates subsidy amounts.

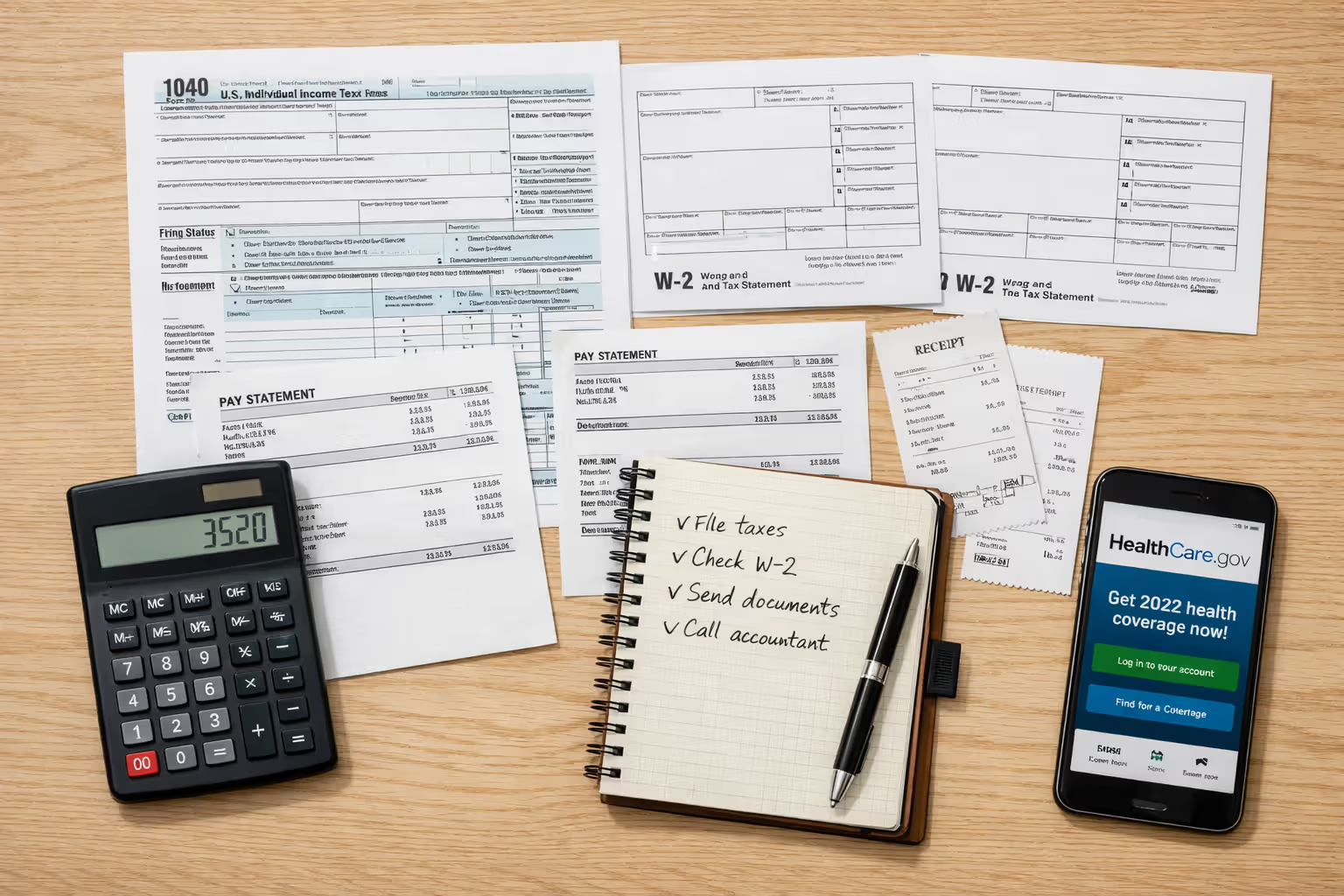

First, collect documentation: recent paystubs, tax returns, W-2s, or profit-loss statements if you're self-employed. Here's what trips people up: the marketplace wants your projected annual income for the upcoming year, not last year's tax figures. Lost your job recently? Got hours cut? Use current income projections, not outdated tax data.

Set up your account on HealthCare.gov (or your state's exchange site) and work through the application. You'll report household size, income sources, and whether anyone's getting offered affordable employer coverage. The calculator instantly determines your subsidy eligibility.

Income reporting demands precision. Count wages, self-employment earnings, Social Security benefits, unemployment payments, investment income, and taxable retirement distributions. Don't include non-taxable Social Security, child support, or monetary gifts. Modified Adjusted Gross Income drives eligibility—it's slightly different from standard AGI on tax forms.

Household size means you, your spouse if filing jointly, and any dependents you're claiming on taxes. This gets messy fast with separated couples, adult kids, or multigenerational living situations. Wrong household size calculations tank your subsidy eligibility or stick you with surprise tax bills.

After comparing available plans, pick coverage and decide how to use your premium tax credit. Option one: advance payments that immediately lower monthly premiums. Option two: pay full price monthly, then claim the entire credit on your tax return. Most people choose advance payments for immediate savings, reconciling everything when filing taxes.

Special enrollment periods grant coverage access outside regular open enrollment if qualifying life events occur: losing other coverage, relocating to a different state, getting married or divorced, having a baby, adopting a child. You've generally got 60 days from the triggering event to enroll. Income changes alone won't open special enrollment, but losing Medicaid eligibility definitely does.

Author: Derek Whitmore;

Source: proactive-coach.com

Mistakes That Can Disqualify You from Financial Assistance

Small application errors or renewal oversights can obliterate your subsidies or generate unexpected tax bills. Knowing the common traps helps you sidestep them.

Income miscalculation tops the error list. Underestimate your earnings and you'll receive excessive advance credits, then owe money back at tax time. Overestimate and you're paying unnecessarily high monthly premiums. Self-employed people struggle most with projections, particularly when business income bounces around. Conservative estimates protect you from repayment obligations—you'll just get the difference back as a tax refund.

Not reporting mid-year income shifts causes major headaches. Scored a raise? Received an inheritance? Started earning more from a side hustle? Update your marketplace application within 30 days. This recalibrates your advance credits to match new income, preventing huge repayment demands. The reverse works too—reporting income drops can immediately boost your subsidies.

Household size mistakes happen when family situations change. Kid leaves for college? Adult child ages off your plan? Elderly parent moves in? Each situation affects household size and subsidy math. Every change should prompt an application update.

Ignoring renewal deadlines terminates your coverage. Marketplaces mail renewal notices each fall, requiring you to review and update information even when nothing's changed. Blow off these notices and you'll lose coverage and subsidies. Automatic renewal technically continues coverage but uses stale information from the previous year, potentially misaligning subsidies with your actual situation.

Taking employer coverage without checking affordability kills marketplace subsidies. If your employer offers coverage considered "affordable" (costing under 9.12% of household income for employee-only coverage), you lose subsidy eligibility—even when adding family members costs a fortune. Some people unknowingly forfeit subsidies by enrolling in employer plans that crush their budget.

Skipping premium tax credit reconciliation at tax time creates IRS problems. Form 1095-A from the marketplace must get reported on your return using Form 8962. Skip this step and you're looking at delayed refunds or IRS inquiries.

State-Specific Programs and Resources for the Uninsured

Federal programs don't tell the whole story. Many states run additional assistance programs for residents falling through coverage cracks.

About 30 states operate pharmaceutical assistance programs that supplement federal prescription help. These programs typically focus on seniors, people with disabilities, or those managing specific chronic conditions. What they cover and who qualifies differs dramatically—some handle Medicare copays, others provide medications to uninsured residents with particular diseases.

Emergency Medicaid covers critical medical situations for individuals meeting all Medicaid requirements except immigration status. Coverage scope stays limited to emergency room treatment, labor and delivery, and emergency dialysis—but excludes ongoing management of chronic conditions or preventive care.

State high-risk pools used to cover people with pre-existing conditions before the Affordable Care Act passed. Most shut down after ACA implementation, though several states maintain reinsurance programs that reduce marketplace premiums across the board by subsidizing enrollees with high medical costs.

Some counties fund indigent care programs delivering basic healthcare to low-income uninsured residents. These county-funded programs typically require proof of residency and income, and may restrict services to specific medical facilities. Coverage quality and eligibility rules vary wildly between counties.

Specialized state programs zero in on particular populations. Multiple states fund family planning services for low-income women outside Medicaid eligibility. Others operate breast and cervical cancer screening programs that unlock Medicaid coverage if cancer gets diagnosed. Tuberculosis and STI treatment programs provide free care across most states regardless of insurance status or immigration documentation.

The coverage gap represents one of healthcare policy's most persistent failures. Working adults—home health aides, restaurant staff, gig economy workers—earn slightly too much for Medicaid in their state yet can't realistically afford $400 monthly premiums on $25,000 yearly incomes. What works in practice? Creative combinations: catastrophic marketplace plans covering disasters, community health centers handling routine care, prescription assistance programs, and aggressive medical bill negotiation. It's far from ideal, but people survive the system when they understand how to work it strategically.

— Dr. Rebecca Martinez

State insurance departments maintain consumer assistance programs helping people navigate coverage options, decode medical bills, and resolve insurer disputes. These free services can uncover programs you never knew existed.

Frequently Asked Questions About Affording Healthcare Without Medicaid

Finding Your Path Forward

Getting squeezed between Medicaid ineligibility and unaffordable marketplace premiums feels like hitting a dead end with no escape routes. Reality? Multiple pathways exist once you know where to look. Solutions rarely involve just one program—most people in your shoes piece together coverage using marketplace subsidies they didn't realize applied to them, community health centers for checkups, prescription assistance for medications, and hospital charity care when unexpected emergencies strike.

Start by checking your real marketplace costs using current income projections. Many assume coverage is impossible based on outdated information or without factoring in enhanced subsidies. If marketplace plans genuinely remain unaffordable, locate health centers near you and establish care before health problems emerge. Preventing medical issues costs dramatically less than treating emergencies.

Don't wait for the perfect solution. Catastrophic coverage protecting you from financial ruin, combined with sliding-scale primary care, beats going completely uninsured. Track your income carefully, report changes promptly, and deploy available resources strategically. The system is fragmented and maddening to navigate, but working through it successfully separates those accessing healthcare from those avoiding medical care until conditions become life-threatening.

Related Stories

Read more

Read more

The content on this website is provided for general informational and educational purposes only. It is intended to offer guidance on pet insurance topics, including coverage options, deductibles, premiums, claims processes, reimbursement models, waiting periods, and related insurance matters. The information presented should not be considered legal, financial, veterinary, or professional insurance advice.

All information, articles, explanations, and policy discussions published on this website are provided for general informational purposes. Pet insurance policies vary widely between providers, and details such as coverage limits, exclusions, reimbursement rates, waiting periods, pre-existing condition policies, pricing, and eligibility requirements may differ depending on the insurer, pet breed, age, location, and the specific terms of an individual policy. Claim outcomes and reimbursement decisions depend on the exact policy language and the circumstances of each case.

While we strive to keep the information accurate and up to date, this website makes no guarantees regarding the completeness, reliability, or accuracy of the content. The website and its authors are not responsible for any errors, omissions, or actions taken based on the information provided here.

Use of this website does not create a professional-client relationship. Pet owners are encouraged to review the official policy documents provided by insurance companies and consult with a licensed insurance professional or qualified veterinarian when making decisions about pet insurance coverage and care for their pets.